It’s that time of year again! The end of the financial year brings the annual ritual of tax time. As our financial lives become more complex with side hustles, working from home, and digital investments, getting your tax return right is crucial. Here is a comprehensive breakdown of what you need to do to prepare, lodge securely, and avoid the most common traps to maximise your financial position.

1. The Golden Rule of Timing: Don't Rush to Lodge!

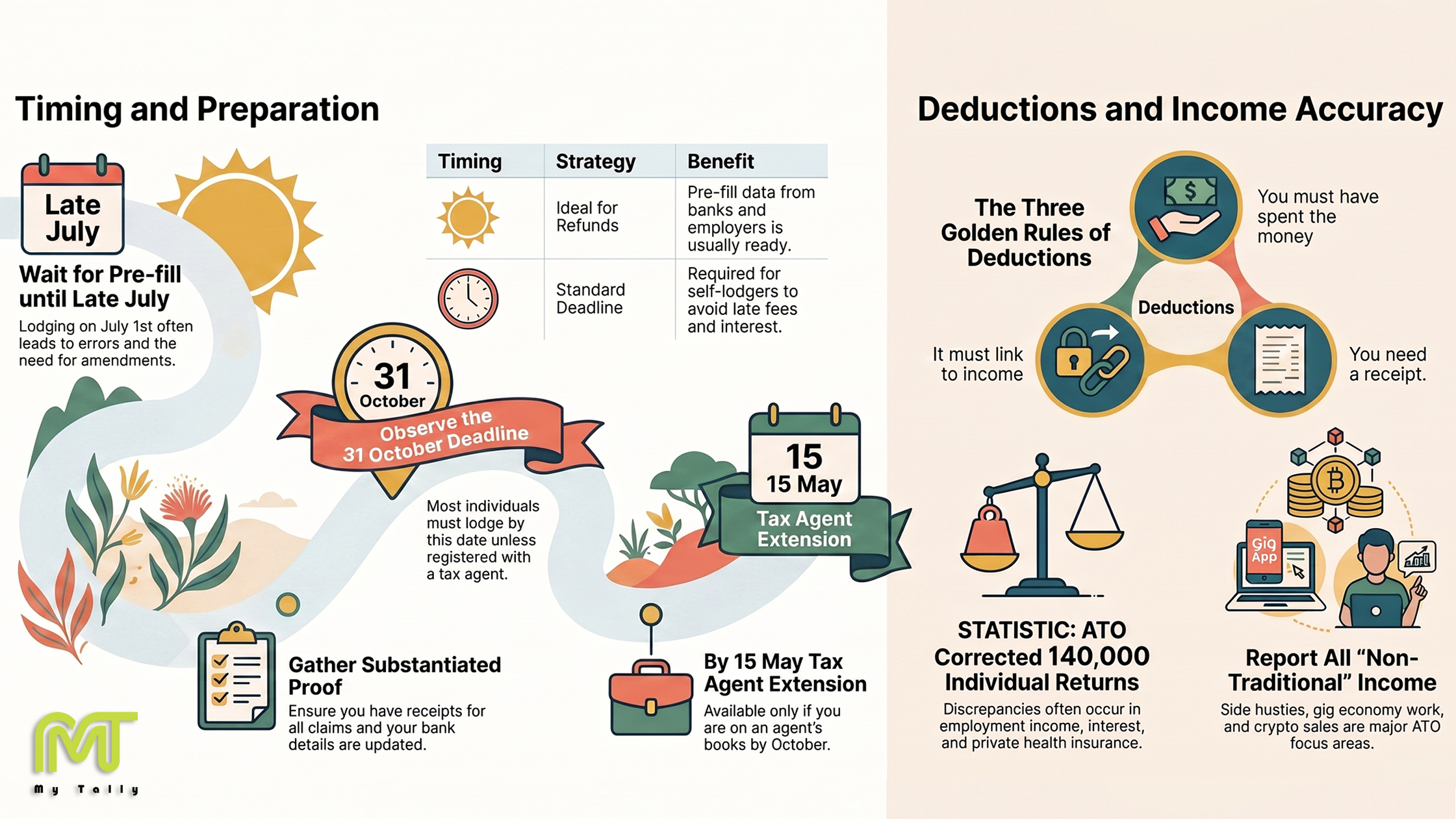

While it might be tempting to get your tax out of the way on July 1, experts strongly advise against lodging too early. The Australian Taxation Office (ATO) uses third-party data from employers, government agencies, banks, and health funds to automatically "pre-fill" your tax return. This information can take until the end of July to become fully available. If you rush, you risk leaving out important information and having to lodge an amended return later, potentially facing interest and fees.

Instead, use early July to prepare: check your myGov access, update your bank details, check if your pre-fill data is available, and gather your receipts. If you are expecting a refund, late July is the ideal time to lodge; if you anticipate a tax bill, you might be better off waiting until just before the October 31 deadline.

2. Make Smart Financial Moves Before June 30

Proper preparation can help you legally minimise your tax and set you up for the new financial year:

- Top up your superannuation: Making additional personal concessional contributions or employee salary-sacrificed contributions can boost your retirement savings and potentially lower your overall tax bill.

- Prepay expenses: You may be able to claim a tax deduction for the current year by prepaying eligible tax-deductible expenses for the upcoming financial year.

- Manage capital gains: The timing of selling investments like shares or managed funds has significant tax implications. Selling a non-performing asset before June 30 might help offset other capital gains.

- Check your health cover: If your income is above a certain threshold, taking out an appropriate level of private hospital cover can help you avoid paying the Medicare levy surcharge.

- Tackle debt and budget: Use this time to set up a savings plan, create a budget, or focus on paying down personal debt and making extra mortgage repayments into an offset account to save on interest.

3. Navigate Deductions Carefully: The 'Three Golden Rules'

The biggest mistake Australians make at tax time is trying to claim things that simply aren't deductible. To legitimately claim a work-related deduction, you must meet three golden rules:

- You spent the money yourself and were not reimbursed by your employer.

- The expense is directly linked to how you earn your income.

- You have a substantiated receipt as proof.

Be aware of common deduction traps. Your daily commute to work is generally private and non-deductible, as are standard workplace clothes like black pants, white shirts, or sneakers. Additionally, if you work from home and use the ATO's fixed-rate method, be careful not to "double dip" by separately claiming the running costs that are already covered by that rate. Rental property owners also frequently stumble by claiming the full interest on a loan partly used for private purposes or claiming renovation costs as immediate repairs.

4. Be Transparent: The ATO Is Watching

The ATO is heavily scrutinising areas where taxpayers make mistakes, particularly omitted income from non-traditional sources like side hustles, the gig economy, cash jobs, and social platforms.

Crucially, investors often forget that selling shares or cryptocurrency triggers a tax event simply by disposing of the asset, regardless of whether the money has actually landed in your bank account. Remember that the ATO already receives extensive data from employers, banks, share registries, property records, and crypto exchanges, and they actively check to see if your return matches their picture.

5. Beware of AI and Influencers

A major warning for this tax season: be very cautious about using Artificial Intelligence (AI) to decide what you can claim. AI might draw on overseas tax rules or outdated information that does not apply to an Australian tax return. Feeding sensitive details like pay slips, bank statements, or your Tax File Number into an AI tool is also a massive privacy risk.

Similarly, avoid taking advice from unregistered social media influencers. If you need help, utilize the ATO's free Tax Help program, National Tax Clinics, or ensure you use a registered tax agent found on the Tax Practitioners Board Register.

6. Lodge Safely and Finalise Government Payments

Most people need to lodge a return or submit a non-lodgment advice by October 31. You can easily lodge online by linking the ATO to your myGov account. If you choose to use a registered tax agent, you can delay lodging until May 15 of the following year, provided you are on their books by October 31.

Finally, do not forget that your tax return is tied to other government services. Whether you lodge a return or submit a non-lodgment advice, completing this step is essential for Services Australia to balance your Family Tax Benefit (FTB), Child Care Subsidy (CCS), and to work out child support assessments.

Sources used in this article:

- Lodging too early and other mistakes people make when doing their taxes - ABC News

- Tips to help prepare for tax time - CommBank

- What to do at tax time - myGov